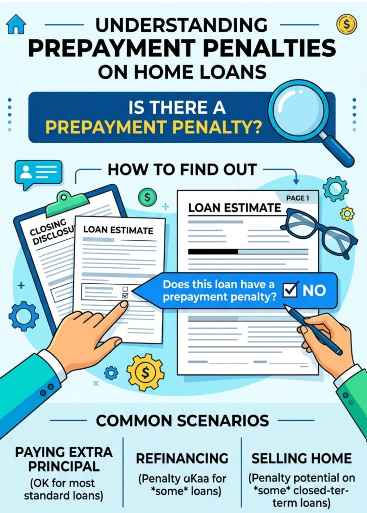

Is there a prepayment penalty on a home loan?

Is there Any Hidden Charges in Home Loans?

How to Compare Home Loan Offers: Complete Guide to Finding the Best Deal

Buying a home is one of the biggest financial decisions you’ll make, and choosing the right home loan can save you lakhs of rupees over the loan tenure. With 25+ banks and HFCs offering home loans in India, comparing offers becomes essential to secure the best deal. Here’s your complete guide to comparing home loan offers effectively. 1. Compare Interest Rates First Interest rates are the most critical factor when comparing home loans. Current rates start from 7.1% p.a. for top lenders. Key Points: 2. Check Processing Fees and Hidden Charges Don’t just focus on interest rates – processing fees and hidden charges can significantly impact your total cost. Charge Type What to Check Processing Fee Usually 0.5%–1% of loan amount Administrative Charges Fixed fees for application processing Legal & Technical Fees Property valuation and legal verification costs Prepayment Charges Penalty for paying off loan early (usually 2%–4%) Part-Payment Charges Fees for making extra principal payments Late Payment Fees Penalty for missed EMI payments Loan Transfer Charges Cost if you want to transfer to another lender later Typical Charges to Compare: 3. Evaluate Loan Tenure Options Loan tenure affects both your EMI amount and total interest payable. Consider These Factors: 4. Assess EMI Flexibility Features Different lenders offer varying EMI flexibility options that can help you save interest. Features to Look For: 5. Compare Loan-to-Value (LTV) Ratio The LTV ratio determines how much of the property value the lender will finance. Key Points: 6. Research Lender Reputation and Service Quality Choose lenders with reputable track records and good customer service. What to Check: 7. Look for Special Features and Benefits Some lenders offer unique features that add value: Special Features to Consider: 8. Use Home Loan Calculators Always use a home loan EMI calculator while comparing rates. Calculate These Metrics: 9. Check Eligibility Criteria Before finalizing, ensure you meet each lender’s eligibility requirements: Common Criteria: 10. Get Multiple Loan Quotes Gather multiple loan quotes before making a decision. Best Practices: Final Tips for Smart Comparison By systematically comparing home loan offers across these factors, you’ll secure the best deal that aligns with your financial situation and long-term goals. Remember, the cheapest loan isn’t always the best – choose the one that offers the right balance of low cost, flexibility, and service quality.

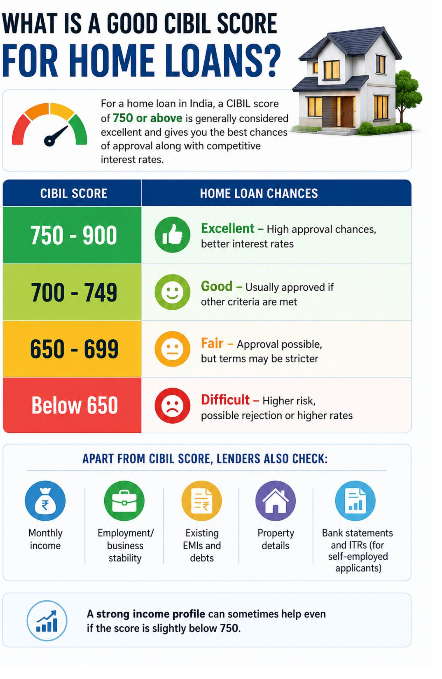

What Is a Good CIBIL Score for Home Loans?

A good CIBIL score not only boosts your loan approval chances but also helps you secure lower interest rates and better loan terms. In this comprehensive guide, we’ll reveal exactly what score you need and how to improve it. What Is a CIBIL Score? CIBIL Score Range Category Home Loan Impact 750–900 Excellent Highest approval chances, best interest rates 725–749 Good Good approval chances, competitive rates 700–724 Fair Approval possible, but slightly higher rates 650–699 Below Average Limited approval,higher rates, may need additional documentation 300–649 Poor Very low approval chances, loan rejection likely A CIBIL score (Credit Information Bureau India Limited) is a three-digit number ranging from 300 to 900 that measures your creditworthiness. It reflects your credit history, payment behavior, debt levels, and credit inquiries. Lenders use this score to assess whether you’re a reliable borrower who’ll repay home loan obligations promptly. What Is a Good CIBIL Score for Home Loans? Key Score Ranges Explained The Ideal Score Generally, an ideal CIBIL score for a home loan is around 700, but this isn’t a strict threshold. However, a score of 750 or above is considered ideal for securing better loan terms and lower interest rates. Why a Good CIBIL Score Matters 1. Higher Approval Chances Scores above 750 significantly improve your loan approval probability 2. Lower Interest Rates Higher scores typically secure better interest rates, saving you lakhs over the loan tenure 3. Better Loan Terms Lenders offer higher loan amounts and flexible repayment options to borrowers with excellent scores 4. Faster Processing Applications with strong credit scores get processed faster with minimal documentation How to Improve Your CIBIL Score If your score is below the desired level, follow these proven strategies: 1. Pay All Debts on Time 2. Reduce Credit Card Balances 3. Avoid Frequent New Credit Inquiries 4. Clear Outstanding Debts 5. Check Your Credit Report Regularly 6. Maintain a Healthy Credit Mix Why Capex Finvest Services Pvt Ltd Can Help Navigating home loan applications with varying CIBIL scores requires expert guidance. Capex Finvest Services Pvt Ltd, specializes in helping borrowers optimize their credit profiles and secure home loans. The team helps clients improve CIBIL scores, compile proper documentation, and connect with lenders offering favorable terms for different score ranges. Final Thoughts A good CIBIL score for home loans is 750 or above, though scores between 700–749 can still secure approval with competitive rates. Start checking your score regularly, pay all debts on time, and reduce credit card balances to improve your creditworthiness. If your score is below 700, consider consulting experienced advisors at Capex Finvest Services Pvt Ltd to navigate alternative lending options and improve your application strength before approaching lenders.

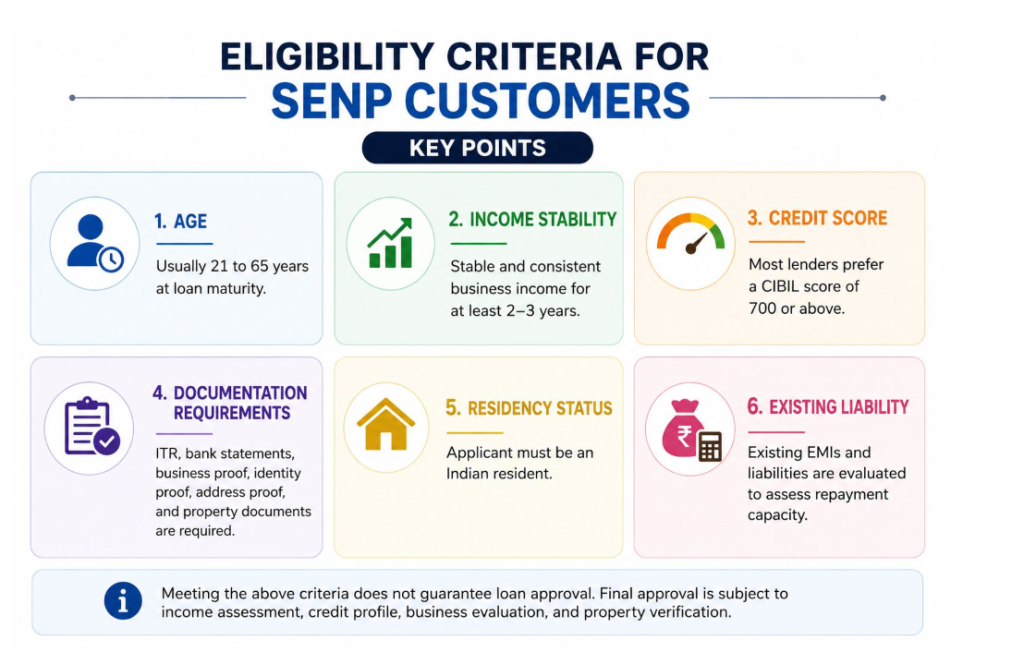

SENP Home Loan with High Turnover but Lower ITR: Can You Still Get Approved?

Many Self-Employed Non-Professional (SENP) borrowers face a common challenge: they have high business turnover but show lower income in their Income Tax Returns (ITR). If you’re a trader, shop owner, or small business proprietor wondering whether this discrepancy will block your home loan approval, the answer is yes—you can still get approved with the right approach and alternative documentation. Why This Gap Exists SENP customers often report lower ITR income due to: However, lenders understand that high turnover indicates business health and repayment capacity, even if taxable income appears low. How Lenders Evaluate High Turnover, Low ITR Cases Key Assessment Factors Factor What Lenders Check Bank Statements 12–24 months of regular income credits showing cash flow GST Returns If available, validates reported turnover CA-Certified P&L Profit & Loss statement certified by Chartered Accountant Business Proof Shop Act, Udyam Registration, Trade License, GST registration Credit Score Minimum 750+ shows clean repayment history Property Documents Clear title deed and approved building plan Lenders like ICICI Bank explicitly state that self-employed borrowers can get home loans without formal income proof if they show gross professional receipts or business turnover. Alternative Income Proof Options If your ITR shows lower income, submit these alternatives: Shubham Housing Finance specifically approves home loans for self-employed without ITR by accepting bank statements or GST records as alternative proof. Navigating SENP home loan applications with high turnover but low ITR requires expert guidance. Capex Finvest Services Pvt Ltd, specializes in helping self-employed borrowers overcome documentation challenges. The team helps clients compile alternative income proof, improve credit profiles, and connect with lenders offering SENP-friendly terms for high-turnover businesses. Tips to Strengthen Your Application 1. File ITR Every Year Even with low income, file ITR consistently. Gaps hurt your loan case badly 2. Keep Bank Accounts Clean 3. Pay Off Existing Debt Clear old loans and credit card bills before applying. This reduces monthly burden 4. Pay More Upfront Paying a higher down payment (beyond 75%–90% loan coverage) reduces lender risk 5. Add a Co-Applicant Bring in a salaried family member (spouse or parent). Their fixed income compensates for uneven earnings 6. Apply for Lower Loan Amount Improves approval chances when income proof is limited Final Thoughts High turnover with lower ITR doesn’t disqualify SENP customers from home loans. Lenders increasingly recognize business turnover as a valid repayment capacity indicator. By submitting alternative documentation (bank statements, GST returns, CA-certified P&L), maintaining a clean credit score, and potentially adding a co-applicant, you can secure approval. Consulting experienced advisors at Capex Finvest Services Pvt Ltd ensures you present the strongest application to lenders who understand SENP profiles.

What are the eligibility criteria for SENP customers?

RBI Repo Rate Stability: Why It Matters for Borrowers, Business & India’s Economy

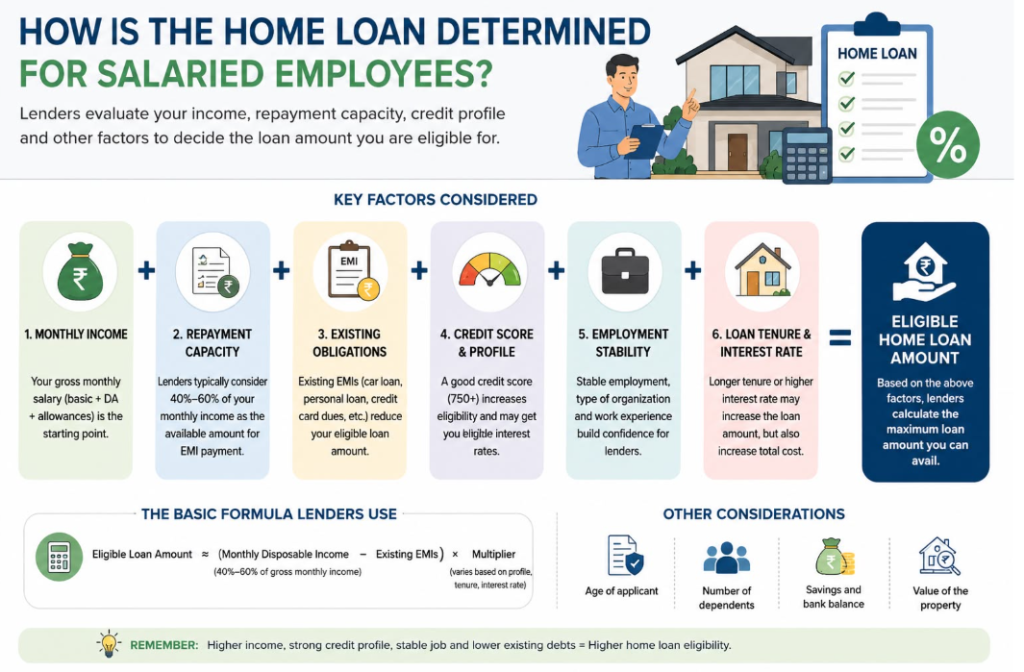

How is the loan amount determined for salaried employees?

What is FOIR and why is it critical?

What non-tax benefits should Home loan customers understand?